The choice of the right insurance policy might vary from one individual to another, as what may suit you might not suit someone else. The choice of plan depends on your financial budget, future financial objectives, policy tenure, coverage offered, premium amount, maturity benefits, etc. While comparing a life insurance & term insurance plan, one can use a Term Insurance Plan Calculator to know which suits you most in terms of premium amount to be paid, benefits to be offered, & coverage provided. In this article, let us understand the difference between the two types of insurance plans, namely, life & term plans.

What is Life Insurance?

Life Insurance is an agreement between an insurance company, i.e., the insurer & an individual, i.e., the insured. Under any specific circumstances, loss, damage or injury occurs to the insured, & this legal bond entitles him to receive the financial security from the insurer.

Hence, the main objective is to offer financial protection to the policyholder & their family. Also, there are some general or non-life insurance policies, where some financial losses are covered, such as travel insurance, health insurance, motor insurance, commercial insurance, marine insurance, etc.

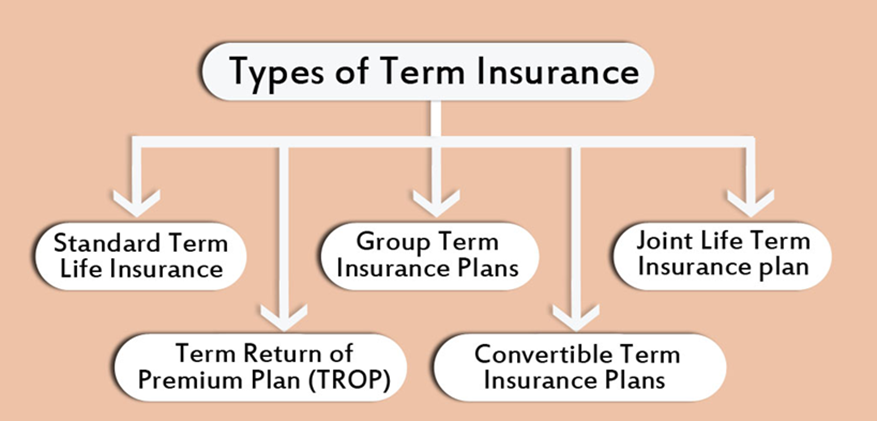

What is Term Insurance?

Term Insurance Plan is a type of life insurance where a specific amount is mentioned to the nominee to be received on the policyholder’s demise. It is a cost-effective life insurance plan that is considered quite useful due to the financial compensation being offered to the dependent family members. A Term Insurance policy is vital as it offers comprehensive life protection coverage to the family members of the policyholder in case of a sudden demise.

Difference between Life Insurance vs. Term Insurance

Provided are the differences between a Life Insurance & a Term Insurance Plan:

| Point of Difference | Life Insurance | Term Insurance |

| Death & Maturity Benefits | This plan offers both death & maturity benefits. | This plan offers only a death benefit, which means providing financial security in case of the untimely death of the policyholder. |

| Tenure | This plan offers an extended period, such as a whole life plan covers policyholders for as long as 100 years. | It comes with a fixed tenure, such as 5, 15, 30, or 35 years. |

| Premium Amount | It offers a higher premium amount as it provides both maturity & death benefits. | It offers a lower premium amount, which is easily affordable despite a low salary. |

| Surrender Value | It offers a savings component along with the surrender value, which depends on the policy tenure. | As they don’t include a savings factor, hence no surrender value as well. |

| Bonus | It includes many different bonuses, such as loyalty addition, guarantee addition, etc. | No additional bonus is offered, as it only includes receipt of the sum assured in case of the policyholder’s death. |

| Flexibility | Very flexible | Not very flexible |

| Risk Covered Vs Savings | It includes coverage to risk, but no component of savings. | It includes coverage to risk as well as a savings component. |

| Tax Benefits | This plan includes taxation benefits on the amount of premium paid & death benefits received. | This plan offers taxation benefits on the amount of premium paid & maturity proceeds. |

| Affordability Comparison | Due to the savings component included, it offers a higher premium cost. | Quite affordable, with higher coverage at a lower premium cost. |

Understanding the Key Factors Affecting the Life Insurance & Term Insurance Plan

Provided are the factors affecting the life insurance & term insurance plan:

- Death & Maturity Benefits

A life insurance plan offers both maturity & death benefits, which means the premium amount paid will be paid either at the maturity date or the policyholder’s death.

A term insurance plan only offers death benefits in case the policyholder dies anytime during the policy tenure.

- Tenure

A life insurance plan offers a longer tenure, which may be up to the life span of the policyholder.

A term plan offers a shorter tenure, such as 5, 15, 30, or 35 years.

- Premium Amount

The premium amount is quite high as it includes both savings & risk components.

As a term plan only includes a pure risk component, the premium amount is generally lower.

- Surrender Value

A life insurance plan helps accumulate a cash value, which is generally paid if the policy is surrendered before the maturity date.

Under the term plan, there is no accumulation of cash value, hence no payout if the policyholder surrenders the plan before the maturity date.

- Tax Benefits

Under both the plans, the premium paid is eligible for a tax deduction u/s 80C & the death benefits received are exempt from tax u/s 10(10D) of the Income Tax Act, 1961.

- Affordability

A life insurance plan is expensive as it covers both risk & savings components. Whereas a term plan is a little cheaper, providing high coverage at a low premium cost.

What to Choose – A Life Insurance or Term Insurance Plan?

You should choose a life insurance plan if:

- You are looking for lifetime coverage with a savings factor.

- You are looking for a plan that offers both maturity & death benefits.

- You can afford to pay higher premiums.

- You are looking for an accumulation of wealth.

You should choose a term insurance plan:

- You are looking for a budget-friendly premium with high coverage.

- You are comfortable with only the insurance plan, i.e. without any savings component.

- You are looking for death benefits that will offer financial security to the family members in case of your demise.

Conclusion

There are multiple factors on the basis of which one can decide whether to buy a life insurance or term insurance plan, such as financial objectives, risk appetite, & financial protection required. Hence, assess your requirements, financial objectives & investment horizon & then choose accordingly. If your main objective is only protection coverage at a reasonable cost, go for a term plan. But if you want some investment factor also to be included, reach out for life insurance plan.